Do banks give fixed-rate loans?

We'll help you finance your dream home. A fixed-rate mortgage offers a straightforward, predictable monthly payment. Your interest rate—and your total monthly payment of principal and interest—will stay the same for the entire term of the loan. That predictability makes it easier to set your yearly budget.

Unaffected by Bank Rate changes, a fixed interest rate could make it easier for you to calculate interest or repayments over time. In terms of borrowing, loans may be offered at a fixed interest rate for the full term. Other types of borrowing may offer fixed interest rates for an introductory or promotional period.

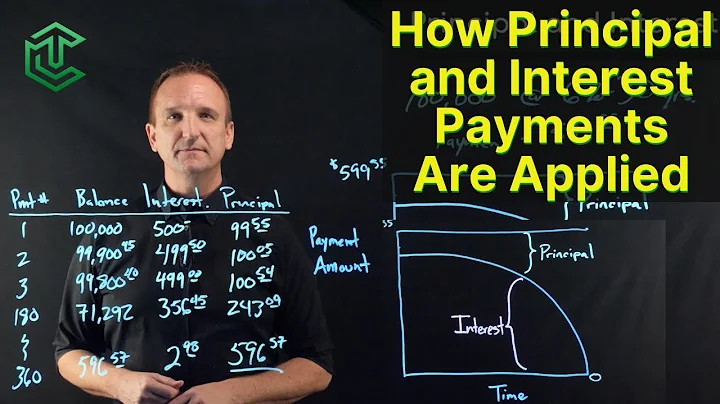

In a fixed-rate loan (also called a term loan), the interest rate stays the same for the loan's entire term. For example, you could have a loan with a 15-year amortization and a five-year term. During that five-year term, the interest rate would be “locked in.”

A fixed interest rate on a mortgage, loan, or line of credit makes it easier to calculate the lifetime cost of borrowing because the rate doesn't change. This allows you to budget for other expenses, including any extras like vacations or a new car. It also gives you the opportunity to plan for any savings.

Fixed-rate loan borrowers can predict their future payments with accuracy since the payments are not affected by future changes in interest rates. Examples of fixed-rate loans include auto loans, personal loans, fixed-rate mortgages, and federal student loans.

Less flexibility: Fixed rate loans may limit a borrower's ability to pay off their loan faster by restricting additional repayments or capping them at a certain amount a year. Significant break fees can apply if you want to refinance, sell your property or pay off your loan in full before the fixed term has ended.

| Banks | Interest on Fixed Deposit | Tenure |

|---|---|---|

| HDFC | 3.00% – 7.00% | 7 days to 10 years |

| Post office | 6.90% – 7.50% | 12 months to 120 months |

| ICICI Bank | 3.00% – 6.90% | 7 days to 10 years |

| Axis Bank | 3.00% – 7.00% | 7 days to 10 years |

Fixed and variable rate home loans

Variable rate home loans tend to be more flexible, with more features (e.g. redraw facility, ability to make extra payments); fixed rate home loans typically do not. Fixed rate home loans have predictable repayment amounts over the fixed term, variable rate home loans do not.

Interest only terms are also available on fixed rate loans - the interest only term must match the fixed rate term. You can have a mortgage offset linked to your home loan if you choose an eligible variable loan like our Clear Path Variable Interest Only Home Loan.

The easiest banks to get a personal loan from are USAA and Wells Fargo. USAA does not disclose a minimum credit score requirement, but their website indicates they consider people with scores below 640, so even people with bad credit may be able to qualify.

What is the average fixed loan rate?

| Product | Interest Rate | APR |

|---|---|---|

| 30-Year Fixed Rate | 6.83% | 6.88% |

| 20-Year Fixed Rate | 6.65% | 6.70% |

| 15-Year Fixed Rate | 6.31% | 6.39% |

| 10-Year Fixed Rate | 6.25% | 6.32% |

The benefit of a fixed-rate mortgage is that your interest rate stays consistent. But your monthly mortgage bill can still change — in fact, it generally fluctuates at least a little bit every year. Rising home values and insurance premiums have caused unusually dramatic increases for some homeowners in recent years.

The primary disadvantage of the 30-year fixed rate mortgage is that you'll probably end up with a higher interest rate compared to a loan with a shorter term or an adjustable mortgage. That's the price you pay for the long-term stability.

The interest rate on the money we borrow is known as the 'cost of funds'. If you make additional repayments, or pay out your fixed rate loan early, the original loan term remains the same. Accordingly, an economic cost is charged to us and this is why we pass this cost on to you.

- Nationwide BS Fixed. Rate. 4.23% ...

- first direct Fixed. Rate. 4.31% ...

- first direct Fixed. Rate. 4.39% ...

- first direct Fixed. Rate. 4.47% ...

- Nationwide BS Fixed. Rate. 4.47% ...

- Yorkshire Building Society Fixed. Rate. 4.49% ...

- first direct Fixed. Rate. 4.54% ...

- first direct Fixed. Rate. 4.58%

You may be able to get a fixed interest rate on various types of loans, including student loans, mortgage loans, auto loans, and home equity loans or home equity lines of credit. However, you won't find many credit cards with a fixed interest rate. Most revolving credit cards instead charge a variable interest rate.

Interest Rate Trends and Forecast: In general, if you think interest rates are going up, locking into a fixed rate agreement is favorable (at least in the short term). If you think interest rates are going down, a variable rate agreement is ideal in the short term.

If you take a variable interest rate it means the rate at which you repay will fluctuate over the term of your home loan, in line with repo rate changes. As a general rule, a fixed interest rate is higher than a variable one because it poses more of a risk for the bank.

The main advantage of a fixed-rate loan is that the borrower is protected from sudden and potentially significant increases in monthly mortgage payments if interest rates rise. Fixed-rate mortgages are easy to understand and vary little from lender to lender.

- As of July 2024, no banks are offering 7% interest rates on savings accounts.

- Two credit unions have high-interest checking accounts: Landmark Credit Union Premium Checking with 7.50% APY and OnPath Credit Union High Yield Checking with 7.00% APY.

Which bank gives 7.75 interest rate?

ICICI Bank fixed deposit rates

The bank offers the highest interest rate of 7.75% for senior citizens on tenure between 15 months to less than18 Months. For individuals, the highest interest rate on FDs can go up to 7.2% on tenure between 15 months to 2 years.

| Institution Name | APY | Compounding Method |

|---|---|---|

| BrioDirect | 5.35% | Monthly |

| TAB Bank | 5.27% | Monthly |

| Newtek Bank | 5.25% | Daily |

| UFB Direct | 5.25% | Daily |

At the present moment, fixing appears less wise for those who are looking for long-term benefits. Fixed rates are relatively high and the cash rate is predicted to reach its peak soon. If borrowers can make the repayments until the cash rate reaches around 4%, it might be better if they stick with variable rates now.

ARMs are easier to qualify for than fixed-rate loans, but you can get 30-year loan terms for both. An ARM might be better for you if you plan on staying in your home for a short period of time, interest rates are high or you want to use the savings in interest rate to pay down the principal on your loan.

Fed hikes have pushed mortgage rates up over the last two years. But the Fed has indicated that it's likely done hiking rates and could start cutting in 2024. Once the Fed cuts rates, mortgage rates should fall even further.