What is the general entry for dividends?

Dividends are paid out of the company's retained earnings, so the journal entry would be a debit to retained earnings and a credit to dividend payable.

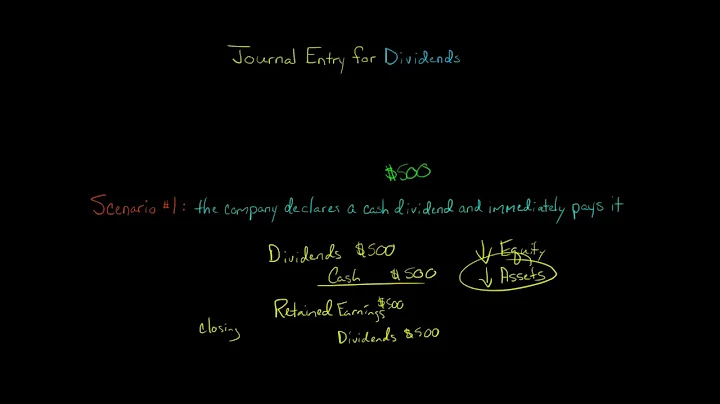

To record a dividend, a reporting entity should debit retained earnings (or any other appropriate capital account from which the dividend will be paid) and credit dividends payable on the declaration date.

A journal entry for a small stock dividend transfers the market value of the issued shares from retained earnings to paid-in capital. Large stock dividends are those in which the new shares issued are more than 25% of the value of the total shares outstanding prior to the dividend.

Dividends paid to shareholders also have a normal balance that is a debit entry. Since liabilities, equity (such as common stock), and revenues increase with a credit, their “normal” balance is a credit.

Cash dividends are paid out of a company's retained earnings, the accumulated profits that are kept rather than distributed to shareholders. The correct journal entry post-declaration would thus be a debit to the retained earnings account and a credit of an equal amount to the dividends payable account.

Treatment of Dividends in Financial Reporting

Under generally accepted accounting principles (GAAP), dividends are not considered an expense of doing business; instead, they are accounted for as a reduction of equity on the balance sheet and added back to net income to compute earnings per share.

A common stock dividend distributable appears in the shareholders' equity section of a balance sheet, whereas cash dividends distributable appear in the liabilities section.

Crediting to Demat Accounts: The DP or RTA then processes the dividend payments and credits the respective amounts into the bank accounts linked to the investors' demat accounts. Notification to Investors: Investors receive notifications or statements from their DPs or RTAs informing them about the dividend credit.

1. If Company X buys shares from Company Y, X becomes the shareholders of Y. So, when dividend is received by X, the double entry is firstly Dr Cash; Cr Dividend (other income), and at the end of year it will be Dr Dividend; Cr Retaining Earnings? 2.

Dividends are not Expenses

When a company pays a dividend it is not considered an expense since it is a payment made to the company's shareholders.

What type of account is dividends?

Both the Dividends account and the Retained Earnings account are part of stockholders' equity. They are somewhat similar to the sole proprietor's Drawing account and Capital account which are part of owner's equity.

Dividend payment is recorded through a reduction in the company's cash and retained earnings accounts as a liability. Because cash dividends are not a company's expense, they show up as a reduction in the company's statement of changes in shareholders' equity.

Any dividend received from the associate is removed on consolidation of the profit or loss and replaced by the share of profit of associate under equity accounting. If there is an outstanding receivable in the SFP then this is not eliminated as it is outside of the group.

Close the dividends account by debiting retained earnings and crediting dividends.

Dividends Declared Journal Entry

Dividends are paid out of the company's retained earnings, so the journal entry would be a debit to retained earnings and a credit to dividend payable.

Balance Sheet: Dividends paid reduce the “Retained Earnings” account under the “Equity” section. When dividends are declared but not yet paid, they may appear as a “Dividends Payable” under “Current Liabilities.”

Dividend voucher: You must provide each shareholder with a dividend voucher. An electronic version is fine, if previously agreed by shareholders, or the company should send out a paper version in the post to each shareholders. The voucher should include: the company name.

Cash Dividends on the Balance Sheet

Investors will not find a separate balance sheet account for dividends that have been paid. However, after the dividend declaration and before the actual payment, the company records a liability to its shareholders in the dividend payable account.

You'll find these in a company's 10-K annual report. Here is the formula for calculating dividends: Annual net income minus net change in retained earnings = dividends paid.

Dividends Payable

In the general ledger hierarchy, it usually nestles under current liabilities. On the date of declaration, credit the dividend payable account. And as with debiting the retained earnings account, you'll credit the total declared dividend value. These two lines make the balance journal entry.

Is dividend an asset or expense?

For shareholders, dividends are an asset because they increase the shareholders' net worth by the amount of the dividend. For companies, dividends are a liability because they reduce the company's assets by the total amount of dividend payments.

Dividends are not reported on the income statement. They would be found in a statement of retained earnings or statement of stockholders' equity once declared and in a statement of cash flows when paid.

A cash dividend primarily impacts the cash and shareholder equity accounts. There is no separate balance sheet account for dividends after they are paid. However, after the dividend declaration but before actual payment, the company records a liability to shareholders in the dividends payable account.

What is the journal entry of a dividend collected by a bank? The journal entry for the dividend collected by the bank is as follows: Bank A/c Dr. Here, Bank Account is debited and the Dividend Received Account is credited …

Dividends typically are credited to a brokerage account or paid in the form of a dividend check. The dividend check is mailed to stockholders but can be direct-deposited to a shareholder's account of choice, if preferred. The alternative to cash dividends is additional shares of stock.